Home Mortgages: What You Required To Know

Content by-Lewis McCoyIf it's time for you to get a home mortgage, then you might feel a little intimidated. You are thinking about the different companies and their products, and you are thinking about your credit. You are probably thinking about the large amount of paperwork and the approval and closing process as well. Don't let these things overwhelm you, but instead focus on the tips that you're about to read and deal with each step one at a time.

Try getting pre-approved for your mortgage. It helps you know what you're able to spend before you bid on properties. It also helps you avoid getting attached to a home that is out of your price range. The process is generally simple: you contact a mortgage lender, submit the personal and financial information, and then wait for their response. Some information in this process will include the amount you can afford and your loan's interest rate. You will receive a pre-approval letter from your lender, and then you'll have the funds as soon as the seller accepts the bid. Your pre-approval process may not be this simple, but it could be.

To make your application for a mortgage fast and easy, make electronic copies of your last two pay checks, two recent bank statements, W2s, and tax information. Lenders will ask for all of this information to go with the application and having them on hand in electronic format makes it easy to supply this information.

Avoid fudging the numbers on your loan application. It is not unusual for people to consider exaggerating their salary and other sources of income to qualify for a larger home loan. Unfortunately, this is considered froud. You can actually be criminally prosecuted, even though it doesn't seem like a big deal.

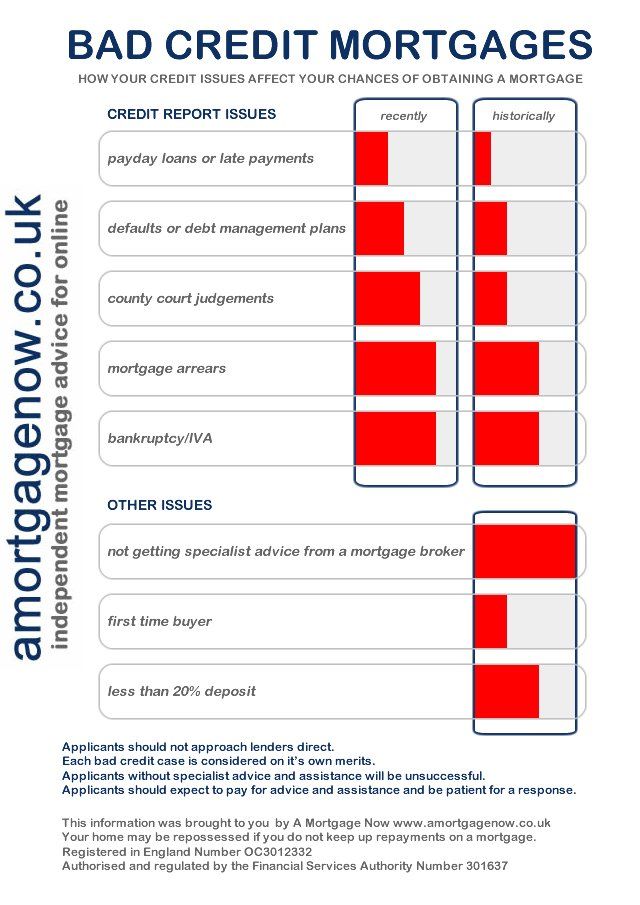

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

Save up for the costs of closing. Though you should already be saving for your down payment, you should also save to pay the closing costs. They are the costs associated with the paperwork transactions, and the actual transfer of the home to you. If you do not save, you may find yourself faced with thousands of dollars due.

Try to have a down payment of at least 20 percent of the sales price. In addition to lowering your interest rate, you will also avoid pmi or private mortgage insurance premiums. This insurance protects the lender should you default on the loan. Premiums are added to your monthly payment.

When financing a house, giving a large down payment will result in a lower mortgage rate. This is due to the fact that a big down payment will reduce your loan to value ratio. When the loan to value ratio gets lower, the interest rates become more favorable for the home buyer.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

When considering a home mortgage lender, check the lender's record with the Better Business Bureau (BBB). The BBB is an excellent resource for learning what your potential lender's reputation is. Unhappy customers can file a complaint with the BBB, and then the lender gets the opportunity to address the complaint and resolve it.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

Make sure that you have a good amount of savings before you get yourself into a home mortgage contract. There are not certainties when it comes to the economy or job stability. To protect yourself you want to have enough money saved to make your payments for many months in case the worst does occur.

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). Each of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

If you need to make repairs to your home you may want to consider a second home mortgage. As long as you have a good history of paying on time you should be able to get a great rate, and by improving your home you are increasing its value. Just be sure that you will be able to make the payments.

Before you apply for a home mortgage, be sure to check your credit score. You can get a copy of your credit report for free once a year from one of the three big credit reporting companies. Check to be sure your credit report is accurate. Correct any problems you find. It is very important to have a clean and positive credit report before applying for a home mortgage.

Don't ever be worried to wait on things for a while in case a better offer on a loan comes up. Suggested Browsing of each year can present different rates. You may find a better option when a new mortgage company opens or when the government passes new legislation. Waiting is frequently in your own best interest.

Ask around about mortgage financing. You may be surprised at the leads you can generate by simply talking to people. Ask your co-workers, friends, and family about their mortgage companies and experiences. They will often lead you to resources that you would not have been able to find on your own.

Be aware that certain things may need to be done to the property before the loan can be approved. One such thing is extra insulation added to the home. This work can either be done by the home buyer or the homeowner. However, once the work is completed, it must be inspected by a certified inspector.

Now how do you feel about mortgages? If click this link are ready to start looking for that mortgage you desire for a home, then this article has motivated you. Remember that you need to be very considerate of all of your options so that you don't make any mistakes. This is a major decision, and the tips that have been given to you should help.